A massive wave of initial public offerings (IPOs) is sweeping across U.S. equity markets at an unprecedented scale, led by some of the most prominent names in space and artificial intelligence.

On June 12, Elon Musk’s SpaceX is set to go public, aiming to raise $75 billion—an amount that would shatter the global IPO record.

Meanwhile, AI heavyweights Anthropic and OpenAI are accelerating their own listing plans. Combined, the three companies are to raise approximately $200 billion.

However, as capital enthusiasm surges, skepticism is rising just as quickly.

Mega IPOs Target $200 Billion in Total

According to an updated prospectus filed on June 3, SpaceX plans to issue approximately 556 million shares at $135 per share, targeting $75 billion in proceeds and implying a valuation of $1.77 trillion.

This would easily surpass the previous IPO record set by Saudi Aramco in 2019, which raised about $29.4 billion.

In parallel, Anthropic confidentially filed for an IPO on June 1 and is expected to list in September. OpenAI is also reportedly preparing for a public offering by the end of the year. Market estimates suggest each company could raise as much as $60 billion.

To accelerate inclusion of these mega-cap listings into major indices—and thereby attract passive investment flows—Nasdaq has shortened the waiting period for newly listed companies to just 15 trading days. FTSE Russell has reduced its timeline to five days, while S&P Dow Jones is reportedly considering similar changes.

Valuation Concerns Intensify

Despite the scale of these offerings, concerns over valuation are mounting.

SpaceX, for instance, reported approximately $19 billion in revenue in 2025, alongside nearly $5 billion in losses. At a valuation of $1.77 trillion, this implies a price-to-sales (P/S) ratio exceeding 90x—an aggressive multiple that many seasoned investors find difficult to justify.

Anthropic and OpenAI face similar scrutiny. Both companies were unprofitable last year, although Anthropic is expected to reach profitability in the second quarter of 2026.

Renowned investor Michael Burry, whose bets against the housing market were featured in The Big Short, has publicly stated that after reviewing SpaceX’s S-1 filing, “nothing in the document supports even a $1 trillion valuation, let alone $2 trillion.”

David Trainer, CEO of investment research firm New Constructs, was even more blunt, calling the current IPO wave “one of the biggest potential scams in history.” He noted that, unlike during the dot-com bubble, investors today may have less choice: rapid index inclusion means millions of retirement accounts could be forced to hold these stocks regardless of valuation concerns.

A Familiar Warning Signal?

Historical patterns add to the unease.

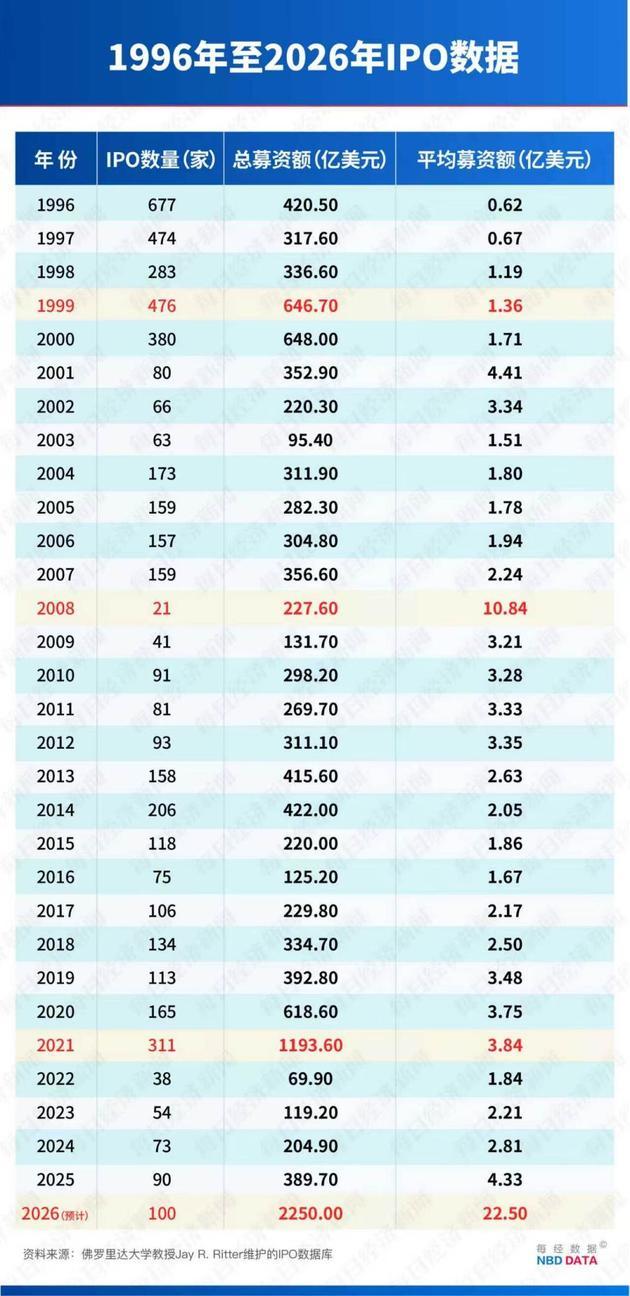

In 1999, U.S. IPO activity surged to 476 deals, raising $64.67 billion—nearly double the previous year—just before the dot-com bubble burst.

In 2008, average IPO size reached $1.084 billion, roughly five times prior years, coinciding with the global financial crisis.

In 2021, IPO fundraising hit a record $119.36 billion, followed by a bear market in 2022.

For 2026, average IPO size is projected to climb to $2.25 billion, with total fundraising nearly doubling the 2021 peak.

Economist Dario Perkins of TS Lombard raised a critical question: if AI is truly transformative, why are companies rushing to share ownership now? The answer, he suggests, may be that insiders believe valuations are near their peak and are seeking to exit while conditions remain favorable.

David Trainer similarly described the IPO surge as a “late-cycle warning signal.”

Post-IPO Performance Often Disappoints

Empirical data also paints a cautious picture.

According to Truist strategist Sam Grelck, IPOs often perform well initially but struggle over time. While returns are typically positive three months after listing, median returns turn negative over six- and twelve-month horizons. In a sample of 30 large IPOs, 19 experienced maximum drawdowns of at least 50% within their first year.

Research by University of Florida professor Jay R. Ritter found that, between 1980 and 2024, IPO stocks underperformed the broader market by an average of 20 percentage points over three years. Companies listing at P/S ratios above 40x underperformed by 58 percentage points. With SpaceX exceeding 90x, its future performance may face significant headwinds.

Liquidity Pressure and Market Impact

The sheer scale of the upcoming IPOs is also raising concerns about market liquidity.

Cash levels among fund managers have fallen to 3.9%, near historical lows, while equity allocations are at their highest in four years. This suggests many investors are already fully invested.

As a result, a large-scale capital rotation may be unavoidable. Investors may need to sell existing holdings to participate in these IPOs, potentially triggering selling pressure in other parts of the market—particularly among large-cap tech stocks.

Paul Kedrosky of MIT’s Digital Economy Initiative warned that many current holdings could face “mechanical selling pressure.”

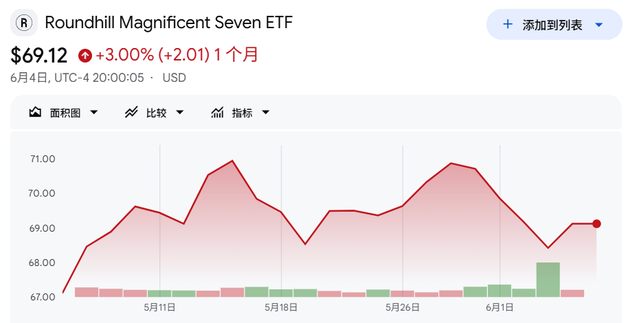

Recent performance trends hint at this “crowding-out effect.” Over the past month, the Roundhill Magnificent Seven ETF rose just 3%, lagging behind the S&P 500’s 4.48% gain and the Nasdaq Composite’s 5.94%.

Meanwhile, sectors such as aerospace (including Boeing and Lockheed Martin), telecommunications (AT&T and Verizon), and even Bitcoin have seen signs of capital outflows.

Blake Anderson, portfolio manager at Carson Group, suggested that these shifts may already reflect investors reallocating capital in anticipation of the SpaceX IPO.

A Divided Outlook

Not all analysts are pessimistic.

Matt Kennedy, a senior strategist at Renaissance Capital, argued that Wall Street has ample capital ready for AI investments. “If a company like Anthropic can raise $65 billion in private markets, it should also be able to do so in public markets without disrupting the broader market,” he said.

Still, whether this historic IPO wave represents a new era of innovation—or a late-stage market peak—remains an open question.

川公网安备 51019002001991号

川公网安备 51019002001991号