On May 22 (local time), Kevin Warsh was sworn in as the new Chair of the Federal Reserve in an ceremony held at the White House and presided over by President Donald Trump—an unusual break from tradition that highlighted rare presidential involvement. Warsh is the first Fed chair since Alan Greenspan in 1987 to take the oath at the White House.

Warsh pledged to lead a “reform-oriented” Fed, while Trump publicly called on him to act as a “fully independent” central banker. However, Trump also said later that interest rates would “come down very soon,” underscoring continued political expectations.

Warsh takes office at a difficult moment. U.S. inflation remains stubbornly high, undermining hopes for rate cuts. Data from the Bureau of Labor Statistics show that April CPI rose 3.8% year-on-year, above expectations and the highest since May 2023. Producer prices climbed even faster, with PPI up 6.0%, the largest increase since December 2022, driven largely by energy.

The shift in inflation has reversed market expectations. Minutes from the Fed’s April meeting revealed four dissenting votes—the most since 1992—with several officials arguing that rate hikes should remain an option. Most policymakers stressed that if inflation stays above the 2% target, further tightening may be necessary.

Fed Governor Christopher Waller, previously seen as dovish, also signaled a shift, supporting the removal of language indicating a bias toward easing. While he said hikes are not imminent, he noted that both rate hikes and cuts are now plausible depending on inflation expectations.

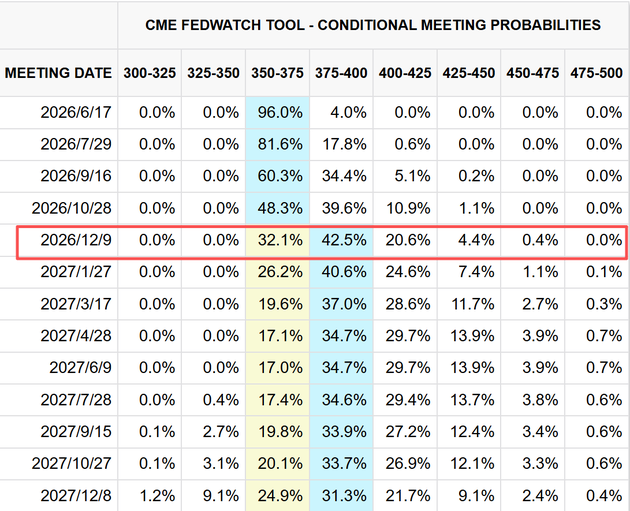

Market pricing reflects this change. As of May 23, CME’s FedWatch tool showed nearly a 70% probability of at least one rate hike this year, effectively ruling out near-term easing.

At the same time, bond markets are already reacting. U.S. Treasury yields have surged, with the 10-year reaching 4.6% and the 30-year briefly exceeding 5.2%, the highest since 2007. The 2-year yield climbed above 4%, signaling expectations that current rates are insufficient to curb inflation.

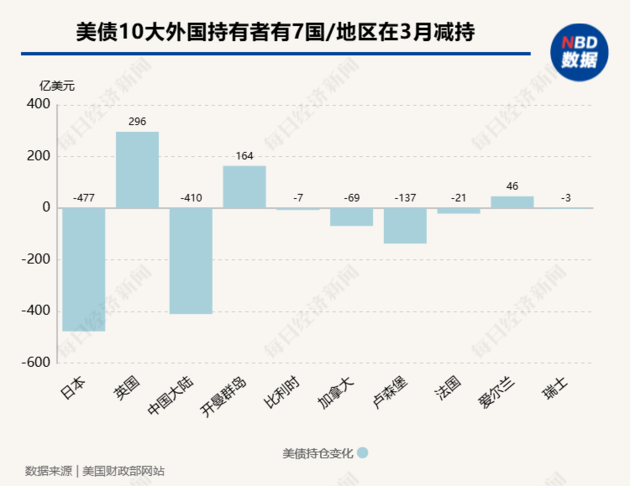

Foreign investors have accelerated their sell-off. In March alone, total foreign holdings of U.S. Treasuries fell by about $138.4 billion to $9.35 trillion. Japan reduced its holdings by $47.7 billion to $1.19 trillion, while China cut $41.0 billion to $652.3 billion, the lowest since 2008. Turkey nearly exited the market, reducing holdings from $16 billion to $1.8 billion.

Warsh has long advocated shrinking the Fed’s $6.7 trillion balance sheet, raising concerns that the policy support underpinning the Treasury market could weaken further.

Adding to the challenge is the “AI paradox.” While Warsh has argued that artificial intelligence could boost productivity and help curb inflation over time, the near-term effect appears inflationary. Massive investment is pushing up costs across the economy.

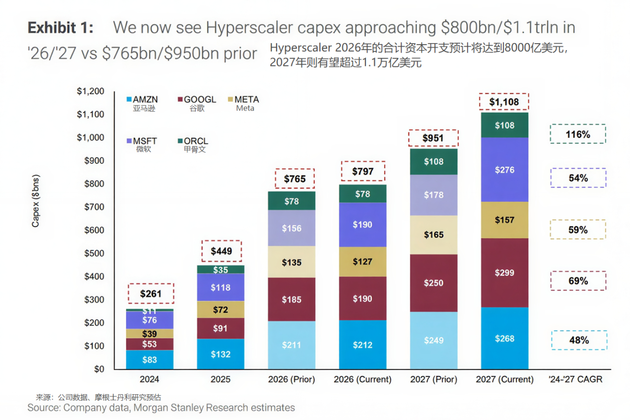

Morgan Stanley estimates that major tech companies—including Amazon, Google, Meta, Microsoft and Oracle—will spend $800 billion on AI infrastructure in 2026, rising above $1.1 trillion in 2027. This surge is driving up prices for chips, computing equipment and electricity. U.S. wholesale prices for electronic components rose 28% year-on-year, while DRAM prices have surged dramatically. Residential electricity prices also increased 4.6%.

To fund this expansion, tech firms are issuing large amounts of debt, further pushing up yields. For example, Meta’s long-term bond yields have risen from 4.65% in 2022 to 6.45% in 2026, significantly increasing financing costs.

As Warsh prepares for upcoming policy meetings, analysts expect the Fed to shift its messaging by removing explicit easing bias and adopting a more neutral stance. This could help anchor inflation expectations and stabilize long-term borrowing costs.

Balancing persistent inflation, bond market volatility, and the unintended effects of AI investment, Warsh faces a complex and narrow policy path at the start of his tenure.

川公网安备 51019002001991号

川公网安备 51019002001991号