With SpaceX on the verge of IPO, how to buy shares in Elon Musk's space exploration company and how retail investors can get in early have become hot topics on social media at home and abroad.

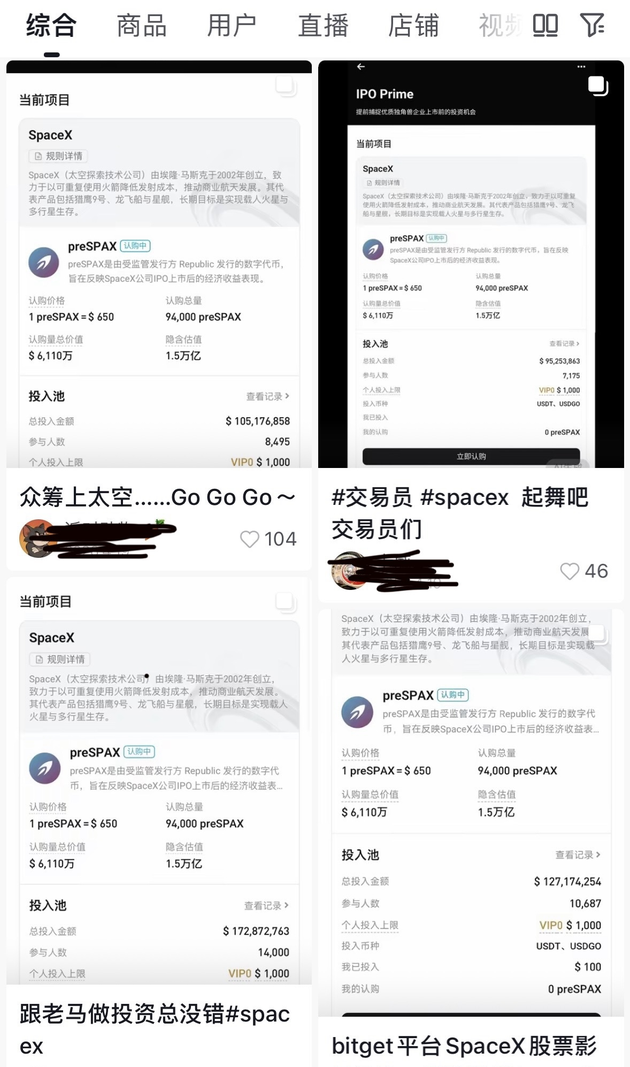

In April this year, preSPAX, a token marketed to provide exposure to SpaceX's post-IPO economic benefits with a minimum entry of just $100 and available only to non-U.S. investors, attracted more than 14,000 investors in just three days, with total subscriptions reaching $177 million (approximately ¥1.2 billion).

However, investors who bought preSPAX do not own actual SpaceX equity, nor are they entitled to dividends or voting rights from SpaceX. The nature of this token and risks from its issuer could lead investors to lose their entire investment.

Over 14,000 Investors Piled Into the "SpaceX Token" With $120 Million

"For just $100, you can bet on SpaceX’s post‑IPO economic upside"—a pitch that seemed to open up pre-IPO access, once limited only to institutions, to ordinary investors.

preSPAX, issued by Republic, a Cayman Islands-based private equity and tokenization firm, sold out rapidly when subscriptions opened on April 18, drawing 4,633 participants within just three hours. When the subscription period ended on April 21, 14,435 investors had participated, with total subscriptions hitting $177 million—about 2.9 times the original offering size.

Bitget acted as the distributor for this token offering, selling tokens to non-U.S. persons in compliant jurisdictions, and served as the designated financial and payment agent for preSPAX.

preSPAX also drew intense attention and discussion on Chinese social media platforms.

Mr. Cheng (pseudonym), a finance‑industry professional, told a National Business Daily reporter:

"I successfully received 9 preSPAX tokens, investing roughly $6,000. I committed about $18,000 in the subscription, and ended up with an allocation ratio of roughly one‑third."

Cheng has followed SpaceX since last year, when IPO rumors first began circulating.

"It's extremely difficult for retail investors to access primary market equity directly," he admitted. "And indirect investments through U.S. ETFs using SPV structures have become way too expensive."

So when he saw a Bitget promotion for preSPAX, he decided to participate out of curiosity.

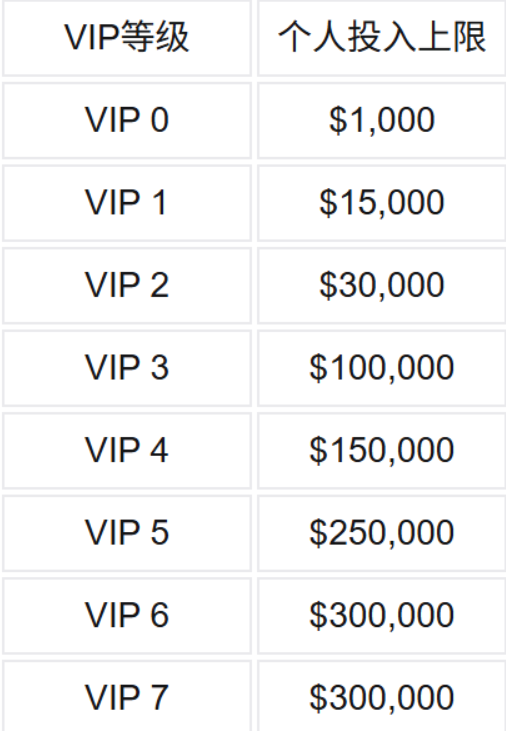

"The entry barrier was low—only $100 minimum. The higher your VIP level, the more you could commit," Cheng said.

According to Bitget's website, the maximum individual commitment for VIP 7 is $300,000.

preSPAX began trading on April 21. On May 25, its price surged to around $930 per token—a 40% increase from the $650 IPO price.

On May 28, Bitget split preSPAX 1:5 and renamed the post‑split token preSPCX, meaning 1 preSPAX became 5 preSPCX.

As of June 1, 14:15 CST, preSPCX was trading at $185 per token. On a pre‑split basis, that equals $925 per token.

preSPAX Price Trend (Note: preSPAX was split 1:5 on May 28)

In early May, after gaining roughly 7%–8%, Cheng sold and exited his position.

"I was just speculating on sentiment, but the price wasn’t moving up earlier. With SpaceX's IPO approaching, there’s a risk of a sell‑off."

But he said he was not surprised by the sharp rally—and felt no regret. He called it purely market hype.

"The $650 issue price corresponded to a $1.5 trillion SpaceX valuation. At $930, the implied valuation exceeded $2 trillion. The speculation is extreme."

The SpaceX Token Is NOT SpaceX Equity — It's Just "Finding the Greater Fool"

The promise of early access to SpaceX excited retail investors. But a core question emerged: Were they buying real SpaceX stock?

Republic and Bitget clearly stated in official announcements: SpaceX is in no way affiliated with the issuance of preSPAX.

preSPAX does not represent actual equity in SpaceX. It only reflects SpaceX’s performance, and holders have no equity, voting rights, or dividend rights whatsoever.

In essence, preSPAX is a Contingent Payout Note—a debt instrument with uncertain payment obligations.

Whether any payment occurs, and how much, depends entirely on future uncertain events.

If preSPAX is not backed by real SpaceX equity, what is the pricing basis for these pre‑IPO tokens?

Ding Yuan, Dean of Firechain Research Institute—a think tank focusing on blockchain, digital assets, and crypto compliance—told NBD, "Based on the product structure in the market, investors are not buying stocks. They are buying derivative contracts that track stock value."

In other words, investors hold nothing more than an IOU from the issuer—with no official connection to SpaceX.

"These products essentially use blockchain to create alternative asset trading venues that traditional finance does not yet offer. They are typical use cases of RWA (Real‑World Assets)," Ding said.

Ding explained that most pre-IPO tokens on the market lack transparent and consistent pricing anchors.

Private transaction prices, secondary market expectations, and market sentiment can all drive pricing.

"When pricing is opaque, the real question becomes: Are you investing or just betting on who will be the next greater fool?"

According to Ding, these tokens carry three major layers of risk:

Underlying asset risk: Whether the platform actually holds sufficient corresponding equity—the foundation of the product's credibility.

Execution risk: If SpaceX's IPO is delayed or canceled, what is the liquidation mechanism? Who sets the price? Who provides downside protection?

Platform risk: If market conditions shift or the platform becomes insolvent, investors could lose all their principal.

No SpaceX Shares as Collateral, No Guarantees — Investors Risk Total Loss

National Business Daily has reached out to issuer Republic to ask about preSPAX’s underlying assets and how its price reflects SpaceX's performance.

As of press time, we have not received a response.

However, the 50-page Offering Memorandum details numerous investment risks for preSPAX.

First, the preSPAX Notes are innovative, tokenized securities with redemption provisions and payout features that differ significantly from traditional debt securities. Though the preSPAX token reflects the economic performance of SpaceX after its IPO, the Offering Memorandum clarifies that no shares of SpaceX common stock underlie the preSPAX Notes, and the preSPAX Notes do not represent an ownership interest, security entitlement, or other direct or indirect interest in any shares of SpaceX common stock. Holders of the preSPAX Notes will have no rights as shareholders of SpaceX, including, without limitation, no voting rights, no rights to receive dividends or other distributions, and no rights to participate in any liquidation or dissolution of SpaceX. SpaceX is entirely unaffiliated with this Offering and has no obligations with respect to the preSPAX Notes.

Meanwhile, the Securities are not deposits and are not insured by the FDIC or any other governmental agency.

In addition, the Issuer is not subject to the reporting requirements of any securities regulatory authority and is not otherwise required to prepare or furnish financial statements in connection with this Offering. As a result, investors will not have access to balance sheets, income statements, cash flow statements, or related notes and disclosures that might ordinarily be available in connection with a securities offering and that are customarily used to evaluate an issuer's financial condition, results of operations, liquidity, capital resources, and indebtedness.

In addition, the Issuer is organized under the laws of the Cayman Islands, and its operations, assets, and management may be located outside of an Investor’s home jurisdiction. Investors may face significant difficulties in enforcing their rights against the Issuer or its directors and officers, as the Cayman Islands may not have treaties providing for reciprocal recognition and enforcement of foreign court judgments, and the legal protections available to creditors and investors under Cayman Islands law may be more limited than those available in other jurisdictions.

川公网安备 51019002001991号

川公网安备 51019002001991号