File photo/ NBD

NVIDIA, the world's most valuable company, delivered impressive earnings after the market closed on Wednesday, August 27th. However, a minor "flaw" of just $200 million instantly rattled the highly sensitive market. In post-market trading, NVIDIA's stock dropped over 5%, and over the next two trading days, its market capitalization evaporated by more than $180 billion.

The reason for this dramatic reaction was a small miss in its data center business revenue for the second quarter of fiscal year 2026. The reported revenue was $41.1 billion, just slightly below the market's expectation of $41.3 billion. For some investors, this $200 million shortfall was like "getting a 98 on a test when everyone expected you to get a 100—it's still a disappointment."

Wall Street's harsh scrutiny of NVIDIA's performance stems from its massive $4.3 trillion valuation. The company has become deeply intertwined with the entire U.S. stock market and the "new engine" of the American economy: AI data center construction. Any signal that deviates from expectations can be magnified, triggering a severe chain reaction.

The Giant Held Captive by "Perfect Expectations"

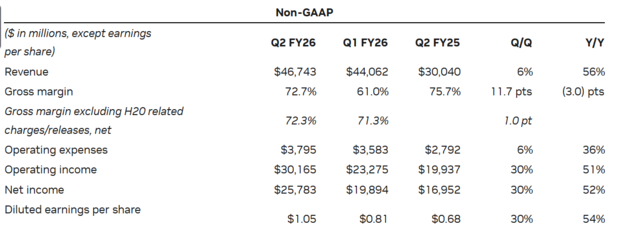

Photo/NVIDIA's earnings report

By any objective standard, NVIDIA's earnings report was brilliant. Quarterly revenue reached $46.743 billion, a 56% year-on-year increase, slightly surpassing the expected $46.23 billion. Its core data center business hit a new high of $41.1 billion, also up 56% year-on-year. Adjusted earnings per share were $1.05, a 54% increase, also beating expectations.

However, these numbers still failed to satisfy Wall Street's "perfectionism." The $41.1 billion data center revenue, which fell short of the $41.3 billion forecast, was immediately interpreted as a sign that cloud computing clients were becoming more cautious with their AI infrastructure spending.

According to Ross Mayfield, an Investment Strategist for Baird Private Wealth Management, the market is so accustomed to NVIDIA's rapid growth that it has developed an irrational "perfect expectation." Any small imperfection is likely to be amplified and trigger an overreaction.

Despite the stock's volatility, analysts remain optimistic. Dan Ives of Wedbush stated that the report is a "guidepost for the tech world" and proves the AI revolution is entering a new growth phase. He expects NVIDIA to reach a $5 trillion valuation by early 2026.

The "NVIDIA Dependency" of the U.S. Stock Market

Some U.S. media outlets suggest that NVIDIA's sustained profitability is more critical to the stock market than whether the Federal Reserve will cut interest rates. This is the underlying reason for Wall Street's strict demands: the entire stock market is increasingly reliant on NVIDIA's performance.

With a market cap of nearly $4.3 trillion, NVIDIA now accounts for 8% of the S&P 500's total market value—a concentration level that, according to the Leuthold Group, surpasses any company they have tracked in the last 35 years. In the tech-heavy Nasdaq 100, its market share is an astounding 14.43%, even higher than Cisco's during the peak of the dot-com bubble.

This unprecedented concentration has a significant impact on the stock market. Passive funds like index funds and ETFs are compelled to continuously buy NVIDIA based on its market-cap weighting. This has created a situation where a massive amount of capital is tied to NVIDIA's stock, making the entire market vulnerable.

According to Apollo Global Management Chief Economist Torsten Slok, NVIDIA alone accounted for 35% of the S&P 500's market cap growth in the first half of the year. SimCorp estimates that a 25% drop in NVIDIA's stock could cause the S&P 500 to fall by 4.4%.

Jensen Huang Photo/VCG

AI Spending: The New Engine of the U.S. Economy

The stock market is a barometer for the economy. As stock indices become more concentrated in AI companies like NVIDIA, the driving force of the U.S. economy is undergoing a historic shift. The "spending spree" on AI data center construction is now replacing traditional consumer spending as the primary engine of economic growth.

Analysts at Renaissance Macro Research estimate that since the beginning of 2025, AI data center spending has contributed more to U.S. GDP growth than consumer spending for the first time in history. Some analysts even suggest that without the AI data center construction boom, GDP could have contracted amid an uncertain macroeconomic climate, suggesting this spending has delayed a potential recession.

The U.S. economy is now deeply tied to NVIDIA, as most AI-related spending flows to the company. NVIDIA's CFO Colette Kress stated that in the last quarter, "large cloud service providers" accounted for about 50% of the company's data center revenue, and data centers represent 88% of NVIDIA's total revenue.

Alphabet, Microsoft, Meta, and Amazon have announced a combined $400 billion in capital expenditures this year, with most of it dedicated to AI infrastructure. NVIDIA’s second-quarter revenue was heavily reliant on two key customers: "Customer A" at 23% and "Customer B" at 16%, for a combined 39% of total revenue. NVIDIA anticipates that total AI infrastructure spending will reach $3 trillion ~4 trillion by the end of the decade.

While NVIDIA has a more solid earnings base and stronger customer relationships than Cisco did during the dot-com bubble, its highly concentrated revenue structure is a significant market risk. When a single company's fate is so tightly woven with the entire market and even a country's economic growth, no investor can ignore the risks that come with such a lofty position. NVIDIA's growth continues, but the "perfectionist" shackles on it are becoming increasingly heavy.

川公网安备 51019002001991号

川公网安备 51019002001991号